NBFC & Lending

Reconciliation for NBFCs, MFIs, and digital lending platforms

Reconciliation in NBFC & Lending

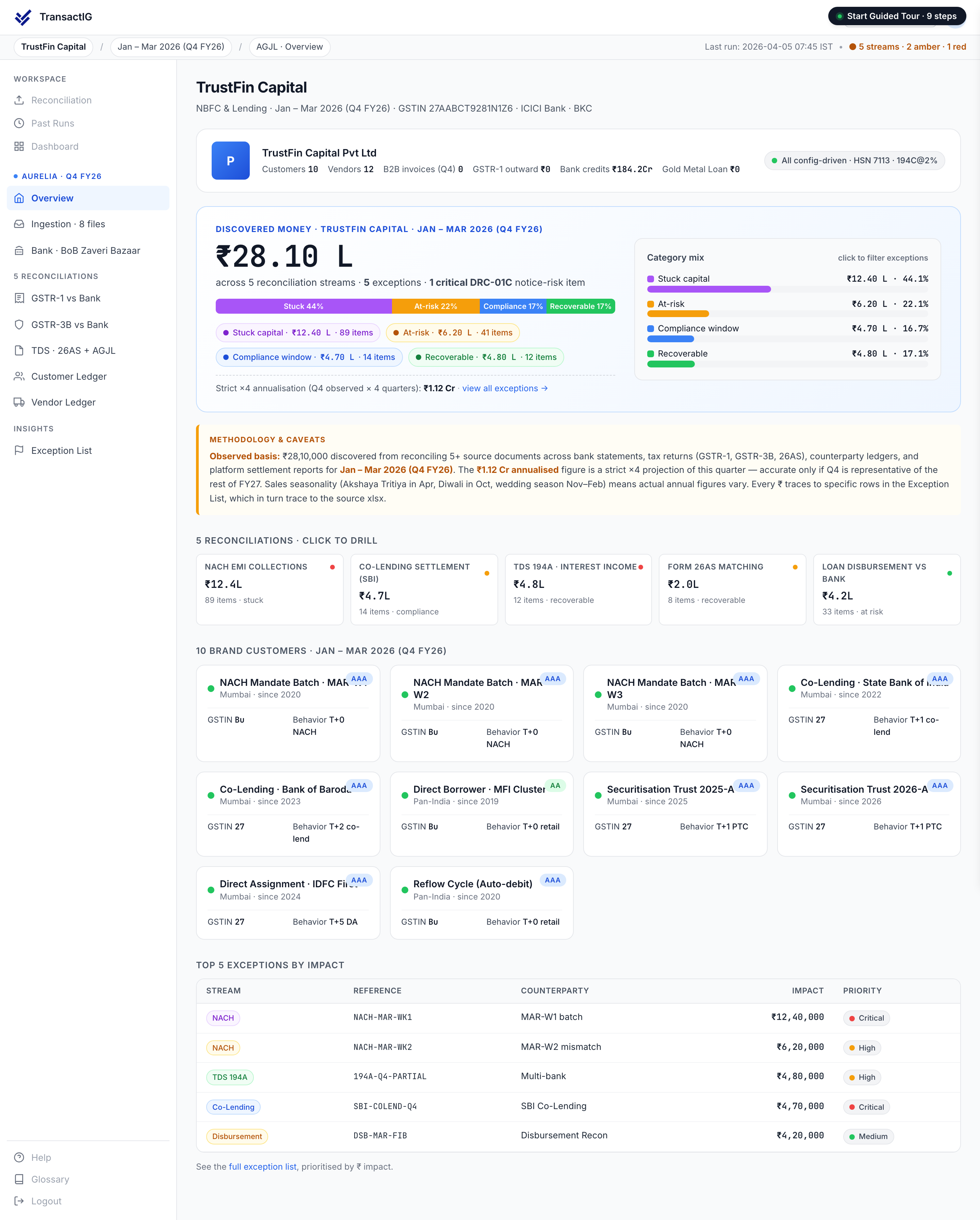

NBFCs and digital lending platforms process thousands of EMI collections daily through NACH, UPI, and direct bank transfers. Co-lending arrangements with banks add another layer — disbursements, collections, and interest splits must be tracked per loan account. TDS deductions on interest income (Section 194A) create a reconciliation obligation that grows with portfolio size. At scale, a mid-size NBFC with 50,000 active loans processes 1.5–2 million collection events per month, all of which must be matched to loan accounts and reflected in the loan management system.

Where reconciliation breaks down

These are the structural problems that generic tools cannot solve for NBFC & Lending businesses.

NACH batch reconciliation at scale

NACH mandates generate batch credits where a single bank entry represents hundreds or thousands of individual EMI collections. Disaggregating a ₹4.5 Cr NACH credit into 2,300 individual loan account credits requires structured batch processing logic — not row-by-row accounting.

TDS on interest income (Section 194A)

Borrowers deduct TDS on interest payments above ₹40,000 per year. NBFCs must track TDS deductions per borrower, reconcile against Form 26AS, and issue TDS certificates — a process that is entirely manual for most LMS platforms.

Co-lending payout reconciliation

Co-lending arrangements with banks require splitting each collection between the NBFC and the bank partner in the agreed ratio, reconciling bank payouts against the agreed split, and tracking interest income separately for each party.

Bounce and part-payment handling

EMI bounces, partial prepayments, and foreclosures generate exceptions that require manual intervention in most LMS systems. At high volume, these exceptions accumulate into a reconciliation backlog that distorts portfolio health metrics.

How TransactIG solves this

TransactIG is built by Terra Insight with nbfc & lending-specific configuration, not generic matching logic.

NACH batch disaggregation

TransactIG matches each NACH batch credit against the mandate file, disaggregates by loan account, and writes back matched status to the LMS — clearing thousands of accounts per batch without manual intervention.

Section 194A TDS tracking

TDS deductions are identified per borrower, matched against 26AS data, and tracked for TDS certificate issuance — automating a compliance process that otherwise requires dedicated headcount.

Co-lending split matching

The co-lending preset applies the agreed split ratio to each collection, reconciles bank payouts against the expected split, and flags deviations for review.

Reconciliation patterns

Configuration presets

No custom development

These presets are included with every NBFC & Lending deployment of TransactIG. Go live in 2–4 weeks.

Regulatory framework

NBFC & Lending reconciliation in India operates within the following regulatory bodies and compliance frameworks.

Frequently asked questions

How does TransactIG handle a NACH batch where some mandates bounce?

Bounced mandates are matched to the corresponding NACH return entries, classified as bounces in the variance taxonomy, and flagged for retry processing — separately from successful collections.

Can TransactIG integrate with our loan management system?

TransactIG integrates with LMS platforms via API or file-based connectors. Common LMS platforms (Finflux, LoanTap, custom platforms) have pre-built integration templates.

We have 200,000 active loans. Can TransactIG handle that volume?

TransactIG is designed for high-volume batch processing. The NACH batch pattern handles millions of transaction records per run without degraded performance.

Does TransactIG handle UPI-based EMI collections in addition to NACH?

Yes. TransactIG supports multi-channel EMI collection matching — NACH, UPI (PhonePe, GPay, BBPS), and NEFT/RTGS — within the same reconciliation run.

Ready to automate NBFC & Lending reconciliation?

Terra Insight will walk you through a live TransactIG demo using nbfc & lending transaction data — matching patterns, variance taxonomy, and ERP integration.