Restaurant Chains

Reconciliation for QSR chains, casual dining, and cloud kitchens

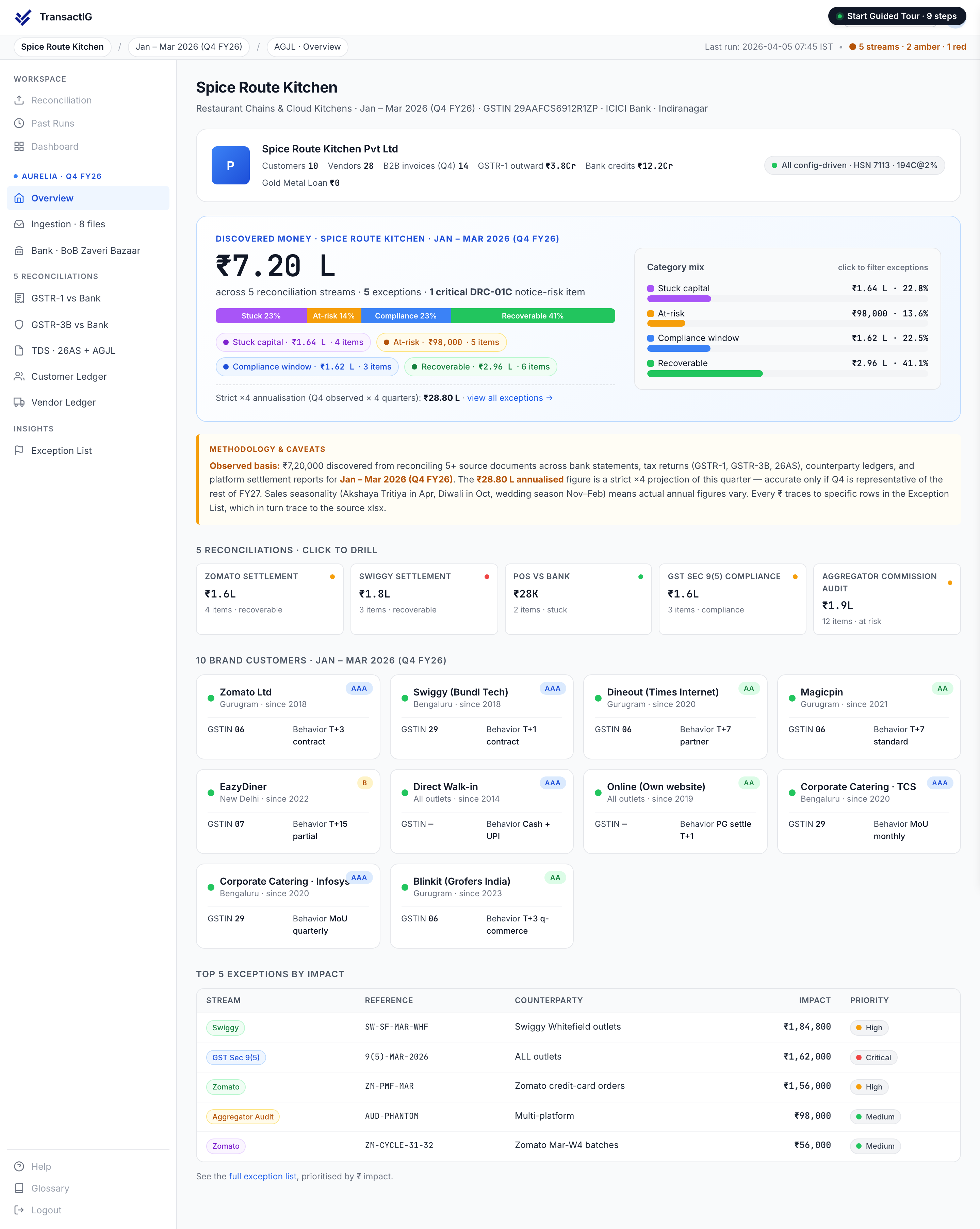

Reconciliation in Restaurant Chains

A multi-outlet restaurant chain in India operates on four reconciliation rails simultaneously. Aggregator settlements from Zomato, Swiggy, Magicpin, and Dunzo arrive net of 25–35% commission plus TDS under Section 393 + payment code 1010 (replacing Section 194O from April 2026) plus TCS at 1% under Section 52 of the CGST Act. POS payment gateway flows via Pine Labs, MSwipe, Razorpay, and PayU settle T+1 to T+3 net of MDR. Daily cash deposits from in-store collection require POS Z-report matching against bank credits. And a GST stream that splits 5% no-ITC for standalone dine-in versus 18% with-ITC for outdoor catering, with hotel-restaurant rates tied to room tariff. Cumulative effect on a typical mid-size chain (50–200 outlets): dozens of distinct reconciliation surfaces with margin leakage that quietly compounds month over month until each rail is closed. Cloud kitchens add another layer — multiple brands operating under one GSTIN, brand-level P&L extracted from a consolidated entity. QSR chains add franchise-royalty reconciliation against franchisor invoices. The category needs reconciliation built around the rails the business actually runs on, not a generic accounting platform that treats aggregator settlements as bank receipts.

Where reconciliation breaks down

These are the structural problems that generic tools cannot solve for Restaurant Chains businesses.

Aggregator commission stack

Zomato and Swiggy weekly settlements bundle 25–35% commission, TDS under Section 393(1)(j) at 1% (replacing 194O from April 2026, payment code 1010), TCS under Section 52 of the CGST Act, and 18% GST on the commission itself — all arriving in one settlement file with no per-order breakdown unless reconstructed.

Section 9(5) GST aggregator liability

Under Section 9(5) of the CGST Act, Zomato and Swiggy pay GST on restaurant supplies on behalf of the restaurant. The restaurant cannot claim ITC on inward supplies attributable to those Section 9(5) sales — requiring a clean split between aggregator-side and restaurant-side revenue for ITC apportionment.

POS payment gateway MDR variance

MDR rates vary sharply by instrument: UPI 0%, debit cards 0.4–0.9%, credit cards 1.5–2%, international cards 2.5–3.5%. A chain processing all four needs different tolerance bands per instrument, not a single MDR rate against a settlement total.

Daily cash deposit close

Cash collection at the outlet flows POS Z-report → cash-room pickup → bank deposit slip — three reference points to match per outlet per day. Common gaps include cash-room shrinkage, voided bills, refund cash-outs, and float adjustments that need a named variance taxonomy.

GST 5% vs 18% split inside one GSTIN

Standalone restaurants pay 5% GST with no ITC on dine-in and takeaway; outdoor catering attracts 18% with ITC; hotel-restaurants are taxed by declared room tariff. The same chain frequently runs all three streams within one GSTIN, requiring sale-line-level GST classification before GSTR-1 filing.

Multi-outlet rollup

50–200 outlets each generate their own POS feed, weekly aggregator settlement, and daily cash deposit. Chain-level P&L cannot be trusted until outlet-level matching closes — and a single misallocated settlement at one outlet pollutes the consolidated number.

Cloud kitchen multi-brand under one GSTIN

A single cloud kitchen runs 5–10 virtual brands on Zomato/Swiggy under one GSTIN. Brand-level P&L (revenue, commission, refunds, spend) must be extracted from a consolidated settlement file using brand identifiers in the order metadata, not from the bank credit alone.

Franchise royalty and inward supply reconciliation

QSR franchisees receive monthly invoices from the franchisor for royalty, national marketing fund, technology fee, and supply-chain margin — each is a separate inward supply with its own GST treatment. Royalty payments attract TDS under Section 393(1)(b) (replacing 194J), so the franchisee-side TDS deduction has to match the franchisor-side credit.

Liquor and bar sales outside GST

Liquor sits outside GST under state excise (FL-3, FL-4 licences) with separate POS or separate billing series, often a separate cash deposit cycle. Mixed bills (food + alcohol) require a clean line-level split before GSTR-1, and many chains discover the split is broken only at audit.

How TransactIG solves this

TransactIG is built by Terra Insight with restaurant chains-specific configuration, not generic matching logic.

Multi-aggregator settlement ingestion

Native ingestion for Zomato, Swiggy, Magicpin, and Dunzo settlement files at order level, with classified deductions for commission, TDS, TCS, refund reversal, ad spend, and SLA penalty — no manual disaggregation of bundled bank credits.

Section 393 + payment code 1010 matching

TDS deducted by aggregators is matched against Form 168 (replaces Form 26AS) on PAN, payment code 1010 (replaces Section 194O), and quarter, with cross-era handling for FY 2025-26 deductions trickling into FY 2026-27 filings.

Section 9(5) GST split rule

A configurable rule per aggregator marks which sales attract aggregator-side GST liability under Section 9(5) and flags the corresponding inward supplies as ITC-ineligible for apportionment, keeping GSTR-3B Table 4 clean.

POS payment gateway feeds with per-instrument MDR

Native ingestion for Pine Labs, MSwipe, Razorpay, PayU, and Paytm-for-Business POS feeds with MDR validation by instrument (UPI, debit, credit, international) — variance is calculated against the contracted rate per instrument, not a blanket MDR.

Daily cash close with named variance taxonomy

POS Z-report, cash pickup, and bank credit are matched per outlet per day, with variances classified as CASH_SHORT, CASH_OVER, VOID, REFUND, or FLOAT_ADJUST so cash-room and finance leadership see the same labels.

Multi-outlet, multi-brand rollup

Outlet-level matching feeds chain-level dashboards with multi-GSTIN consolidation, franchise vs corporate-owned outlet segmentation, and cloud-kitchen brand-level P&L extraction from the same source data.

Production track record

Customers have moved from a 51% to an 88% match rate on equivalent volumes. ISO 27001:2022 certified, AWS Mumbai region, 24+ industry presets, typical 2–4 week implementation.

Reconciliation patterns

Configuration presets

No custom development

These presets are included with every Restaurant Chains deployment of TransactIG. Go live in 2–4 weeks.

Frequently asked questions

How does Section 9(5) of the CGST Act affect ITC for restaurants on Zomato/Swiggy?

When Zomato or Swiggy pay GST on restaurant supplies under Section 9(5), the restaurant cannot claim ITC on inward supplies attributable to those sales. TransactIG flags Section 9(5) revenue at the order level so ITC apportionment between aggregator-side and restaurant-side sales is auditable in GSTR-3B Table 4.

How is the new Section 393 + payment code 1010 different from old Section 194O for aggregator TDS?

From April 2026, the Income Tax Act 2025 replaces Section 194O with Section 393(1)(j) and payment code 1010 for e-commerce operator TDS, and Form 168 replaces Form 26AS. The TDS rate (1%) is unchanged. Section 52 of the CGST Act (1% TCS by aggregators) is GST law and is not affected by the Income Tax Act changes. TransactIG handles cross-era matching where FY 2025-26 deductions trickle into FY 2026-27 filings.

We run 80 outlets across 4 GSTINs. How does multi-outlet rollup work?

Each outlet is a unit with its own POS, aggregator, and cash feeds. Matching closes at the outlet level first, then rolls up by GSTIN for GSTR-1/3B, then by entity for chain-level P&L. Franchise vs corporate outlets are segmented separately so the franchisor royalty calculation does not pollute corporate-store margin.

We run 6 cloud-kitchen brands from one kitchen under one GSTIN. Can we get brand-level P&L?

Yes. Brand identifiers in the Zomato/Swiggy order metadata are used to allocate revenue, commission, refunds, ad spend, and SLA penalties at the brand level. The kitchen-level P&L (rent, kitchen staff, common utilities) is allocated by configurable rules — typically revenue share or order count — to give a brand-level contribution margin.

How does the daily cash deposit close work for an outlet?

Three reference points are matched per outlet per day: the POS Z-report total, the cash-room pickup slip, and the bank deposit credit. Variances are labelled CASH_SHORT, CASH_OVER, VOID, REFUND, or FLOAT_ADJUST. The same taxonomy is used by cash-room, area manager, and finance, so a 0.3% recurring CASH_SHORT pattern at one outlet shows up the same way to all three roles.

How do we keep liquor sales separate when food and bar are billed together?

Liquor is outside GST and tracked under state excise. TransactIG keeps liquor sales on a separate revenue line tied to the FL-3 or FL-4 licence and POS series, with a clean split on mixed bills before GSTR-1 generation. The bar cash deposit cycle, often separate from food cash, is reconciled on its own rail.

How is franchise royalty TDS handled — has the section changed?

Royalty payments to a franchisor that were previously under Section 194J fall under Section 393(1)(b) from April 2026. TransactIG matches the franchisee-side TDS deduction against the franchisor-side credit on Form 168 by PAN, the new payment code, and quarter. Royalty, NMF, and technology fee are tracked as separate inward supplies because each has its own GST treatment.

Do we need to migrate POS or accounting systems to use TransactIG?

No. TransactIG ingests POS exports, aggregator settlement files, payment gateway settlements, and bank statements as they are produced today. It sits beside the POS and accounting systems rather than replacing them, with a typical 2–4 week implementation for a multi-outlet chain.

Ready to automate Restaurant Chains reconciliation?

Terra Insight will walk you through a live TransactIG demo using restaurant chains transaction data — matching patterns, variance taxonomy, and ERP integration.